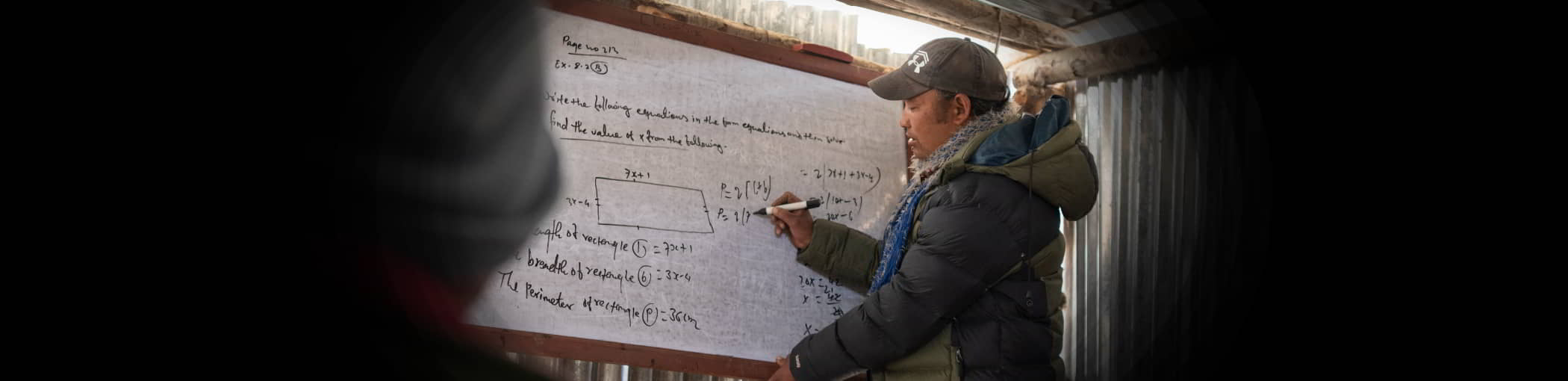

Understanding the Numeracy Definition and its Relation to Poverty

Along with basic reading and writing, one of the key abilities needed to overcome poverty is numeracy skills. The numeracy definition per Merriam-Webster is the “ability to understand and work with numbers.”1 This doesn’t necessarily entail something as complex as algebra. Someone just needs to recognize numbers and be able to perform simple addition and subtraction. In contrast, the inability to do basic math is known as financial illiteracy.

The link between illiteracy and poverty has long been proven.2 Now, organizations recognize that they must also include numeracy as a complementary skill to reading and writing. In 2017, a report by NEFE, a financial education organization, indicated that one in five U.S. teenage students did not have basic math skills.3 This number is staggering in a country where education is fairly ubiquitous. Worldwide, only one-third of adults understand simple math.4 South Asia as a region has the lowest financial literacy rates in the world.5

Factors that lead to this financial illiteracy include lack of access to education, generational poverty and gender inequality. Though there may be a school nearby, if a family is struggling just to survive, there will be no extra money for school fees or supplies. Often, children may be forced to work as young as possible in order to earn income and help the family survive. Girls, in particular, face child marriage and social disparity that commonly excludes them from education. These factors, which are often cyclical, keep children out of school and away from learning. Most likely, their parents can not read or write, let alone know basic math. If this cycle continues, the children and parents can easily become trapped by it.

In addition, illiterate people face money lending schemes.

“A major consequence to the lack of financial literacy in developing Southeast Asia is the rise in thriving loan sharks’ businesses. In Thailand, millions of the poorest and most illiterate become prey of unscrupulous and organized black market lenders who cash in up to 20 percent interest on a small loan—per month.”6

Families may see a loan as the way out of their financial dilemma but end up becoming indentured servants when they are unable to pay back the loan. If they had basic math and literacy skills, they could have understood what they agreed to. Instead, they tie their family’s fate to something they cannot understand.

Being able to avoid that fate, as well as even buy food at the market without being taken advantage of, are essential to breaking cycles of poverty that trap generations of people worldwide.

Preshti lived this cyclical reality of poverty for decades before help came. She grew up poor and illiterate and experienced its effects on a daily basis. When traveling to see her mother, she couldn’t tell which bus to take. She couldn’t read street signs, pay bills, check her earnings or count the change she received at the market when buying her family food. Often, she used her fingerprint to sign legal documents she couldn’t read.7

Then, at 45 years old, Preshti had the opportunity to join reading and financial literacy classes for adults given by GFA missionaries. She was eager to learn but faced many challenges. The GFA workers kindly moved the literacy classes to evenings so Preshti could keep working, but she was exhausted after a day of work, which made it difficult to concentrate. But Preshti persevered.

After completing the classes, her confidence soared in her newfound literacy and now knowing the numeracy definition: understanding numbers! With this newfound strength, Preshti joined other women in a small business plan. It required a loan that Preshti and the other women clearly understood because of their literacy and numeracy skills. Preshti was able to work and pay off the loan, carefully keeping a clear record of her loans and payments. Most importantly, she was providing for her family.

Preshti thought she just needed to read and write, but her basic math skills unlocked even greater potential for her and her family, especially her children. Without GFA World’s literacy classes, Preshti and her family would likely have remained locked in the cycles of illiteracy and poverty. Instead, simple skills became life-changing skills.

GFA World understands the practical benefits of literacy in providing necessary skills for life. They also understand the heart and mind benefits of such skills. Preshti likely would have never considered starting her own business before acquiring literacy and numeracy skills. Being cared for and mentored by GFA missionaries was essential to taking that next step of confidence.

Consider giving to GFA World’s literacy efforts. GFA missionaries have personally witnessed the dilemmas caused by illiteracy and the power of people gaining literacy. They also spread Christ’s love and hope as they help lift individuals and families out of poverty. This doesn’t just change them. It changes their whole communities. Be a part of this gift of literacy today. Your care and compassion, shown through your giving, changes more than one life.

Learn more about Bible verses about poverty

1 “Numeracy.” Merriam-Webster. Accessed February 14, 2022. https://www.merriam-webster.com/dictionary/numeracy.

2 “Literacy Overview.” UNESCO. Accessed February 14, 2022. https://en.unesco.org/themes/literacy.

3 “Report: 1 in 5 U.S. Teens Lack Basic Financial Literacy Skills.” NEFE. May 24, 2017. https://www.nefe.org/news/2017/05/report-1-in-5-u.s.-teens-lack-basic-financial-literacy-skills.aspx?gclid=Cj0KCQiAmKiQBhClARIsAKtSj-nBO8LrdLx68S6hgvTEmTj9K29ZgoVAJq-R7AQxLt6KLTXmxxJ4gYYaAiAgEALw_wcB.

4 Fu, Chang. “32 Must-Know Financial Literacy Statistics in 2021.” Possible Finance. February 15, 2021. https://www.possiblefinance.com/blog/financial-literacy-statistics/#:~:text=Financial%20Literacy%20Statistics%20Overview%3A,7%20Americans%20are%20financially%20illiterate.&text=In%202020%2C%20states%20that%20required,by%2024%20percent%20from%202018.

5 “South Asia has world’s lowest financial literacy.” Investvine. Accessed February 14, 2022. https://investvine.com/south-asia-has-worlds-lowest-financial-literacy/financial-literacy-graph/.

6 Welsh, Brianna Lee. “The Challenges of Financial Literacy in Southeast Asia.” Medium. November 20, 2018. https://medium.com/@briannaleewelsh47/the-challenges-of-financial-literacy-in-southeast-asia-c355fecd7daf.

7 “Literacy Opens Business Opportunities for Women.” GFA World. 13 August 2020. https://gospelforasia-reports.org/2020/08/literacy-opens-business-opportunities-woman/.